Implementation of Tax in Indonesia from the Perspectives of Muhammadiyah and NU

DOI:

https://doi.org/10.12928/jampe.v4i2.13200Keywords:

Implications, Law , Muhammadiyah, Nahdlatul Ulama, TaxAbstract

Taxes remain a widely-discussed topic. It is because taxes are not only limited to state finances but also play a crucial role in a country’s development. This study examines the implementation of taxes (Tax Law, Education Tax, and Tax Amnesty) in a country from the perspectives of Muhammadiyah and Nahdlatul Ulama (NU). This study aims to provide scientific contributions and fill the gap regarding the role of Islamic organizations, specifically Muhammadiyah and NU, in Indonesia, in terms of tax implementation. This study employs the library method as its research approach. The method involves collecting information from laws and regulations, as well as books and articles related to state regulations and the statements or decisions of organizations. The results of the study indicate that Muhammadiyah and NU share the same view regarding tax law. They consider taxes mandatory. For the VAT on education, Muhammadiyah and NU disagree. It is because they also consider it to be contrary to the spirit of Pancasila and the welfare of the people. Furthermore, Muhammadiyah agrees with tax amnesty. However, Muhammadiyah continues to provide input and suggestions to the government. On the other hand, NU has not reached an agreement on the tax amnesty law. Upon examining previous decisions, it was found that NU did not permit Tax Amnesty. This study contributes to the formulation of more inclusive and equitable public policies by integrating the religious perspectives of Muhammadiyah and NU on the implementation of taxes in Indonesia. Thus, it will increase the legitimacy, compliance, and trust of the Muslims in the national taxation system.

References

Abd Rahman, A. B. ., & Rahim, A. B. A. (2020). Were the early firaq extremists? Rethinking the history of muslim disagreement(s). Journal of Islamic Thought and Civilization, 10(1), 46–65. https://doi.org/https://doi.org/10.32350/jitc.101.03

Adam. (2021). PPN Pendidikan Tidak Sejiwa dengan Konstitusi Pancasila. Muhammadiyah.

Adinugraha, H. H., Surur, A. T., & Achmad, D. (2024). Enhancing the Legal Framework: Optimizing Zakat as an Income Tax Deduction in Indonesia. Al-Ahkam: Jurnal Ilmu Syari’ah Dan Hukum, 9(2), 130–153. https://doi.org/10.22515/alahkam.v9i2.10212

Ahmad, F. (2021). PBNU Tolak Rencana Pemerintah Pungut Pajak dari Pendidikan dan Sembako. NU Online.

Ajlouni, A. T. (2017). Interest free liquidity management scheme (time-weighted debt units). International Journal of Islamic and Middle Eastern Finance and Management, 10(1). https://doi.org/https://doi.org/10.1108/mf.2008.00934jaa.001

Al-Hafiz, K. (2016). Bahtsul Masail Mauquf, PBNU Bahas Ulang Tax Amnesty Sumber: https://nu.or.id/nasional/bahtsul-masail-mauquf-pbnu-bahas-ulang-tax-amnesty-hUR0s. NU Online.

Al-Munawir AW. (1984). Al-Munawir: Kamus Arab– Indonesia. Ponpes Al-Munawir.

Al-Munawir AW. (1997a). Al-Munawir: Kamus Arab– Indonesia. Pustaka Progressif.

Al-Munawir AW. (1997b). Kamus Al Munawwir. Pustaka Progressif.

Ali, M. (2021). Relevansi Konsep Perpajakan Menurut Abu Yusuf Dan Ibnu Khaldun Terhadap Perekonomian Di Indonesia. Jurnal Al-Idārah, 2(1), 1–21.

Alm, J., Martinez-Vazquez, J., & Wallace, S. (2009). Tax amnesties and tax collections in the Russian Federation. Economic Analysis & Policy, 39(2).

Amin, M. (2003). Hasyiyah Ibnu Abidin. Dar Al-Kutub.

Antara. (2016). PBNU “Gagal” Rumuskan Hukum Tax Amnesty. Tirto.Id.

Avida, N. H., & Ernandi, H. (2024). Tax Compliance Among Individual Taxpayers in the Digital Era. Indonesian Journal of Law and Economics Review, 19(4). https://doi.org/10.21070/ijler.v19i4.1239

Bentil, J. (2018). Situating the International Tax System within Public International Law. Georgetown Journal of International Law, 49(May 2009), 1219.

Biro Komunikasi dan Layanan Informasi/BKLI, D. P. (2016). Amnesti Pajak, Sarana Menuju Kemandirian Bangsa. Ekon.Go.Id.

Diomande, O. (2020). Fundamentals of Islamic Finance and Easy Access to Credit. Theoretical Economics Letters, 10(4).

Direktorat Jenderal Pajak. (2025a). Amnesti Pajak. Ditjen Pajak.

Direktorat Jenderal Pajak. (2025b). Asas Pemugutan Pajak. Ditjen Pajak.

Direktorat Jenderal Pajak. (2025c). Asas Pengenaan Pajak. Ditjen Pajak.

Direktorat Jenderal Pajak. (2025d). Fungsi Pajak.

Direktorat Jenderal Pajak. (2025e). Jenis Pajak. Ditjen Pajak.

Direktorat Jenderal Pajak. (2025f). Pengertian Pajak. Ditjen Pajak.

Direktorat Jenderal Pajak. (2025g). Sistem Perpajakan. Ditjen Pajak.

Endah, Purnama, V. (2024). Analisis Perbandingan Tax Amnesty Jilid I dan Tax Amnesty Jilid II Pada KPP Pratama Bandung Bojonagara. AKUNESA, 12(3).

Firdaus, M. (2019). Tinjauan Syariah Terhadap Pengalokasian Dana Pajak Di Indonesia. Jurnal Sketsa Bisnis, 6(1), 59–67.

Fitriya. (2024). Pajak Pendidikan dan Ketentuan Pengenaan Pajaknya. Klik Pajak.

Galih, A., & Witono, B. (2024). Digital Transformation and Taxpayer Compliance : A Study of Key Factors Based on Maqasid Syariah Principles. 8(1).

Gangl, K., & Torgler, B. (2020). How to Achieve Tax Compliance by the Wealthy: A Review of the Literature and Agenda for Policy. Social Issues and Policy Review, 108–151. https://doi.org/https://doi.org/10.1111/sipr.12065

Gao, Y., Li, J., & Wu, Y. (2025). Competition and tax avoidance: Evidence from quasi natural experiment of the implementation of Anti-Trust Law. International Review of Economics and Finance, 98(March 2024), 103900. https://doi.org/10.1016/j.iref.2025.103900

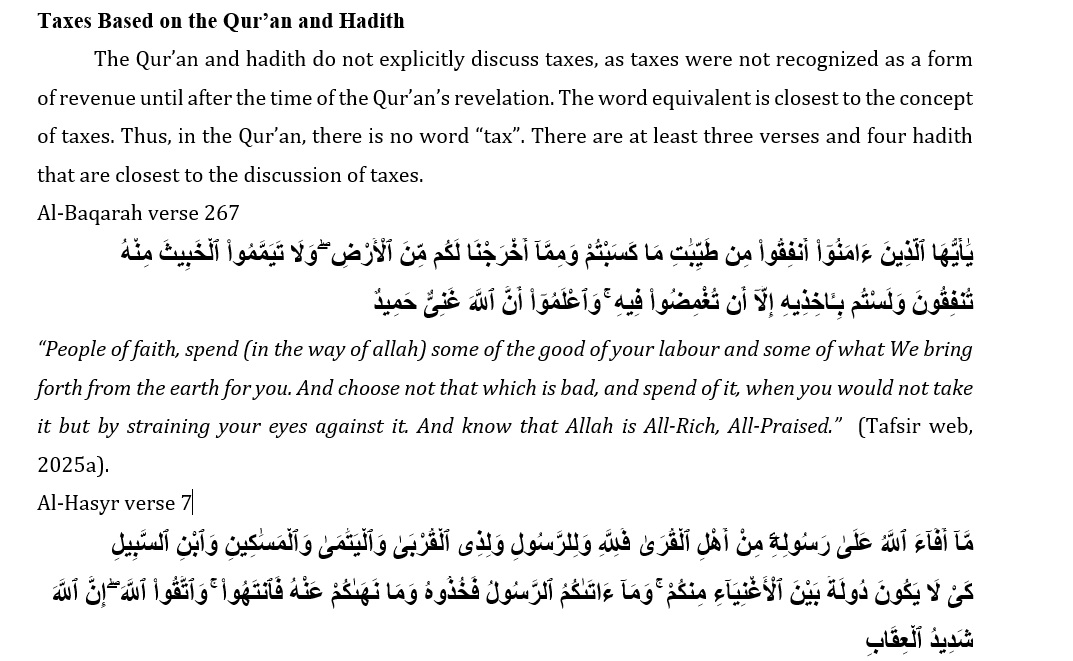

Hakim, R. (2021). Konsep Pajak Dalam Kajian AL-Qur’an Dan Sunnah. Tafakkur, 2(1), 36–48.

Hallaq, W. B. (2009). Authority, Continuity and Change in Islamic Law. Cambridge University Press.

Hazm, I. (n.d.). Maratibul Ijmak. Darul Afaq Al-Jadidah.

Imam, G. (1998). Al-Mustasfa min `Ilmi Al-Ushuli (1st ed.). Dar El-Hadis.

Ispriyarso, B. (2019). Keberhasilan Kebijakan Pengampunan Pajak (Tax Amnesty) di Indonesia. Keberhasilan Kebijakan Pengampunan Pajak (Tax Amnesty) Di Indonesia, 2(1), 47–59.

Jacobsen Kleven, H., Knudsen, M. B., Kreiner, C. T., Pedersen, S., & Saez, E. (2011). Unwilling or Unable to Cheat? Evidence From a Tax Audit Experiment in Denmark. Econometrica, 79(3), 651–692. https://doi.org/10.3982/ecta9113

Jahan, S. (2021). Zakat versus Taxation as Islamic Fiscal Policy Tool. International Journal of Islamic Economics, 3(01), 37–46. https://doi.org/10.32332/ijie.v3i1.3129

Karim, A. (2002). Sejarah Pemikiran Eonomi Islam (2nd ed.). Pustaka Pelajar.

Kismayanti, T. (2025). Penerimaan Pajak Indonesia Masih Ringkih, Bambang Brodjonegoro Soroti Ketergantungan pada Basis Pajak Terbatas. Wartakinni.

Kopczuk, W., Peichl, A., & LaLumia, S. (2018). Introduction to the special issue. International Tax and Public Finance, 25(6), 1401–1403. https://doi.org/10.1007/s10797-018-9520-5

Lubis, I. (1994). Ekonomi Islam Sebuah Pengantar (1st ed.). Radar Jaya Offset.

Luitel, H. (2013). Causes of State Tax Amnesties: A Review. https://doi.org/https://doi.org/10.2139/ssrn.2238902

Madjid, S. S., Amri, U., & Aidil, A. M. (2024). Taxes in the Perspective of Islamic Law. Hukum Islam, 7(1).

Manan, M. (1993). Teori & Praktek Ekonomi Islam,. PT. Dana Bhakti Wakaf.

Meirison, M. (2022). Zakat dan Pajak dalam Tinjauan Para Pakar dan Ulama Kontemporer. Saqifah: Jurnal Hukum Ekonomi Syariah, 11–21. https://journals.fasya.uinib.org/index.php/saqifah/article/view/257%0Ahttps://journals.fasya.uinib.org/index.php/saqifah/article/viewFile/257/145

Mutakin, A. (2021). Fiqh Perkawinan Beda Agama di Indonesia: Kajian atas Fatwa-Fatwa NU, MUI dan Muhammadiyyah. Al-Ahwal: Jurnal Hukum Keluarga Islam, 14(1), 11–25.

Nnamani, O. C., Ifeanacho, K. P., Onyekwelu, E. I., & Ogbuefi, P. C. (2023). Barriers to effective property tax reform in Nigeria: Implementation of the land use charge in Enugu state. Land Use Policy, 126.

Permatasari, Mutiara Intan. (2025). Pajak dalam Sejarah Islam: Dari Kewajiban Terpilih Menjadi Tugas Bersama. NU Online.

Priyono, A. P., Nisa, F., & Dwijayanti, A. (2024). Optimizing Indonesian Tax Collection with Effectiveness and Efficiency Analysis through Transformation to Improve National Welfare. International Journal of PERTAPSI, 2(2).

Qadim, Zallum, A. (2002). Sistem Keuangan di Negara Khilafah. PustakaThariqul Izzah.

Qurthubi, I. (2003). Jami` Li Ahkamil Qur`an (2nd ed.). Dar Al-Kutub Al-Imiyah.

Ra’na, I. (1990). Sistem Ekonomi Pemerintahan Umar Ibn Khattab (1st ed.). Pustaka Firdaus.

Rahayu, Ita, S. (2001). Tinjauan Hukum Islam Terhadap Penegakan Hukum Pajak oleh Lembaga Paksa Badan Gijzeling. Shautuna, 2(107), 118.

Rahayu, I. S., & Wijaya, A. (2021). Tinjauan Hukum Islam Terhadap Penegakan Hukum Pajak oleh Lembaga Paksa Badan Gijzeling. Shautuna: Jurnal Ilmiah Mahasiswa Perbandingan Mazhab Dan Hukum, 107–118. https://doi.org/10.24252/shautuna.v2i1.18144

Ribas. (2016). Pernyataan Resmi PP Muhammadiyah Terkait UU Tax Amnesty. Suara Muhammadiyah.

Sabiq, S. (1999). Fiqh as-Sunnah. Dār al-Fath Lil I‘lām al- ‘Arabi.

Saidi, M. (2010). Perlindungan Hukum Wajib Pajak Dalam Penyelesaian Sengketa Pajak. PT. Raja Grafindo Persada.

Setianingrum, A., Rusydiana, A. S., & Fadhilah, P. R. (2019). Zakat as a Tax Credit for Raising Indonesian Tax Revenue. International Journal of Zakat, 4(1), 77–87. https://doi.org/10.37706/ijaz.v4i1.110

Setyawan, D. (2017). Moving Ijtihad and Tajdid on Amal Usaha Muhammadiyah (Aum) in Building the Civilization of Islamic Economy. Addin, 11(1), 77. https://doi.org/10.21043/addin.v11i1.1904

Sidang Majellis Tarjih dan Tajdid PP Muhammadiyah. (2011). Fatwa Tarjih Tentang Pajak.

Siregar, S. & S. (2017). KEBIJAKAN TAX AMNESTY DALAM PERSPEKTIF EKONOMI ISLAM. Al-Muamalat, 2(2), 1–18.

Suchman, M. . (1995). Managing Legitimacy: Strategic and Institutional Approaches. Academy of Management Review, 20(3), 571–610. https://doi.org/https://doi.org/10.5465/amr.1995.9508080331

Surahman, M. (2017). Konsep Pajak dalam Hukum Islam. Amwaluna, 1(2), 166–177.

Tafsir web. (2025a). Al-Baqarah ayat 267. Tafsir Web.

Tafsir web. (2025b). Al-Hasyr ayat 7. Tafsir Web.

Tafsir web. (2025c). At-Taubah ayat 29. Tafsir Web.

Waluyo, I. (2000). Perpajakan Indonesia. Salemba Empat.

Weber, M. (1968). Economy and Society: An Outline of Interpretive Sociology. Bedminster Press.

Wijayanti, P., Amilahaq, F., Muthaher, O., Baharuddin, N. S., & Sallem, N. R. M. (2022). Modelling zakat as tax deduction: A comparison study in Indonesia and Malaysia. Journal of Islamic Accounting and Finance Research, 4(1), 25–50. https://doi.org/10.21580/jiafr.2022.4.1.10888

Winataputra, Udin, dkk. (2016). Kesadaran Pajak dalam Pendidikan Tinggi. KemenristekDikti dan Ditjen Pajak.

Zuchroh, I. (2022). Zakat Produktif: Kebijakan Pengelolaan Keuangan Publik sebagai Instrumen Pengentasan Kemiskinan di Indonesia. Jurnal Ilmiah Ekonomi Islam, 8(3), 3067–3073.

Zuchroh, I. (2024). Analisis Konseptual Dan Implikasi Praktis Pajak Dalam Konteks Ekonomi Syariah: Sebuah Kajian Interdisipliner. Jurnal Intelek Dan Cendikiawan Nusantara, 1(1), 204–210.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2025 Wahyu Tri Wibowo, Budi Jaya Putra

This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License.